USW Members Make Their Voices Heard! House Passes Protect…

Current Actions

Rapid Response Info Alert: Balancing the Scales: Retirement Security

Rapid Response Action Call: Our Fight to Protect Our…

Rapid Response Action Call: Restore Collective Bargaining Rights for…

Rapid Response Feedback Report: USW Led Critical Victory to…

Rapid Response Action Call: Our Steelworkers Don’t Have Time…

Building Worker Power

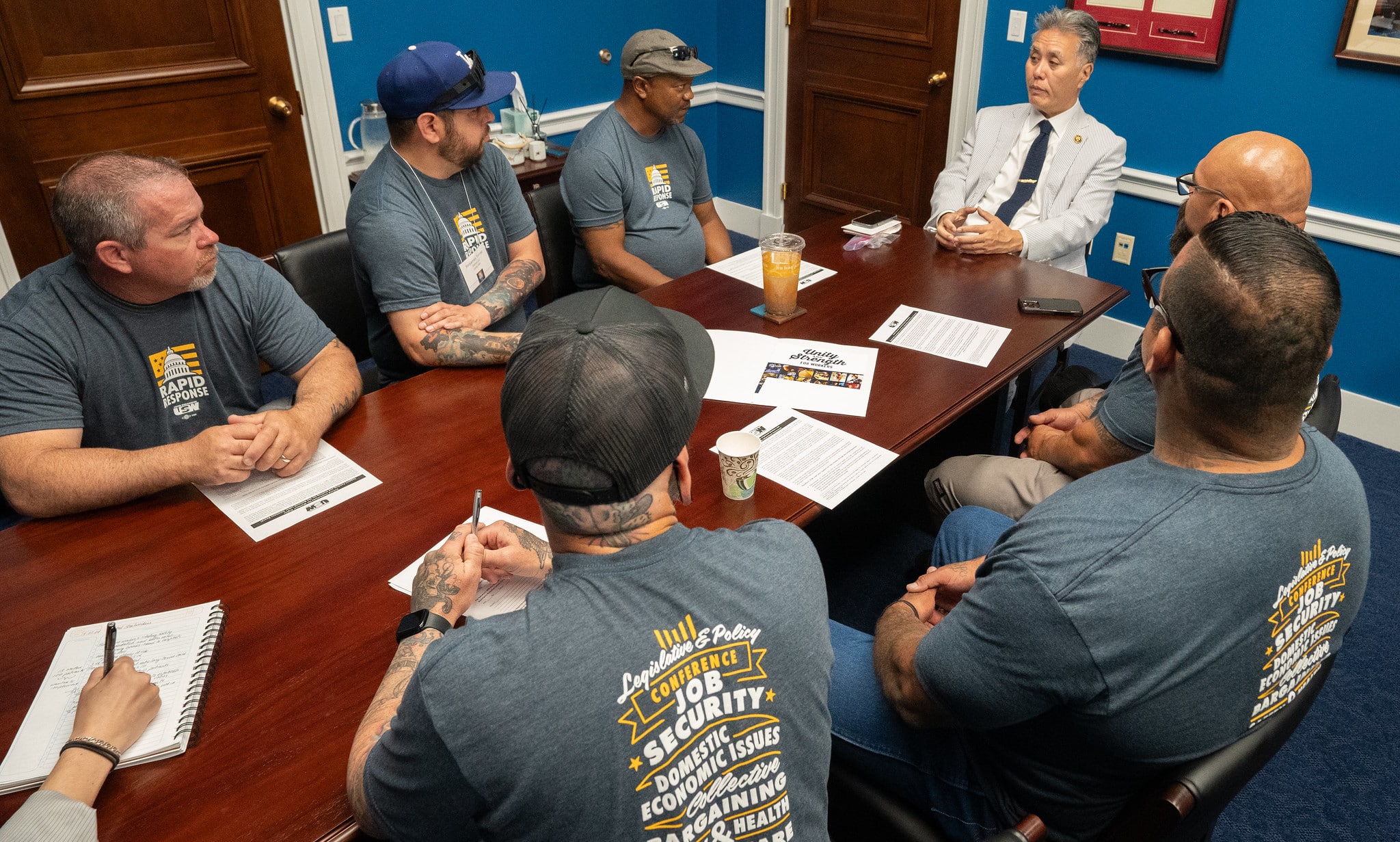

Rapid Response is the Steelworkers’ nonpartisan grassroots education, communication and action program. It informs members about pending labor and work-related legislation, from advancing health and safety to protecting our right to bargain strong contracts. Through Rapid Response, all USW members have a voice in government decisions and legislative actions that affect them, their workplaces and their communities.

Upcoming Events

Stay Connected

Want a voice in government decisions? Sign up for Rapid Response to stay updated on important current legislative issues that could impact our lives.

Amber Miller

Director, Rapid Resonse

Get Rapid Response Updates in Your Inbox

Want to Learn More?

See how the USW is making a real difference in our communities and our workplaces.